Transformative Flow: The Impact

of Remittances on the Banking Sector

Liseth Palomino Salazar

https://orcid.org/0009-0007-3640-1534

UNACEM Group, Finanzas Corporativas, Perú

Angeline Zamudio Salazar

https://orcid.org/0009-0001-1676-0771

Banco de Desarrollo de América Latina y El Caribe, Perú

Received: May 29, 2025 / Accepted: August 25, 2025

https://doi.org/10.26439/ddee2026.n008.7946

This is an open access article, published under the terms of the Creative Commons Attribution 4.0 International (CC BY 4.0) license.

ABSTRACT. This study examines the causal links between remittance flows from abroad and the development of the banking system in Peru, using quarterly data from 2001 to 2024. A two-stage least squares (2SLS) model was employed to address endogeneity and make efficient use of the data. Remittances were found to have a significant positive impact on the development of the banking system by stimulating deposit and credit growth, improving solvency, and strengthening financial margins across banking institutions. In addition, foreign direct investment (FDI) and gross fixed capital formation were also found to contribute positively by facilitating the expansion of financial services. Gross domestic product (GDP) growth and trade liberalization are highlighted as factors that promote banking development by increasing the demand for financial services and fostering international competition. On the other hand, inflation was shown to have a negative impact by reducing the stability of the financial system, underscoring the importance of policies aimed at mitigating its adverse effects.

KEYWORDS: banking sector / remittances / two-stage least squares

Flujo transformador: el impacto de las remesas

en el sector bancario

RESUMEN. Este estudio analiza los vínculos causales entre el flujo de remesas provenientes del extranjero y el desarrollo del sistema bancario en el Perú, utilizando datos trimestrales del período 2001 a 2024. Se emplea un modelo de mínimos cuadrados en dos etapas (2SLS) para abordar la endogeneidad y aprovechar eficientemente la información disponible. Se encontró que las remesas tienen un impacto positivo y significativo en el desarrollo del sistema bancario al estimular el crecimiento de los depósitos y del crédito, mejorar la solvencia y fortalecer los márgenes financieros de las instituciones bancarias. Asimismo, se identificó que la inversión extranjera directa y la formación bruta de capital fijo también contribuyen positivamente al facilitar la expansión de los servicios financieros. El crecimiento del PIB y la liberalización del comercio se destacan como factores que promueven el desarrollo bancario al incrementar la demanda de servicios financieros y fomentar la competencia internacional. Por otro lado, se evidenció que la inflación tiene un efecto negativo al reducir la estabilidad del sistema financiero, lo que subraya la importancia de implementar políticas para mitigar sus efectos adversos.

PALABRAS CLAVE: sector bancario / remesas / mínimos cuadrados en dos etapas

JEL CODES: F24, G21, C58

1. INTRODUCTION

In the past year, remittance flows have experienced remarkable growth in Peru, increasing by about 23 % in the last quarter and reaching 1,7 % of gross domestic product (GDP) (Banco Central de Reserva del Perú [BCRP], 2024). Likewise, in Latin America, these flows reached USD 156 billion, growing by 8 % in 2023 (World Bank, 2023). This upward trend in external capital flows has spurred a growing body of research analyzing their effects on economic growth, inequality, and poverty. However, the literature has paid relatively less attention to the relationship between remittance inflows and the financial system, despite the latter’s central role in channeling and transforming these resources into productive uses.

On the one hand, part of the literature emphasizes that remittances can foster financial development by increasing bank liquidity and deposits, thereby strengthening the intermediation capacity of banks and facilitating credit expansion. Moreover, if these flows are tapped by the banking sector, they can help reduce the financial gap and boost private investment (Aggarwal et al., 2011). In contrast, several studies also argue that these flows may have a limited impact on banking development if they are used exclusively for consumption or if recipient households prefer other means of savings because they do not trust financial institutions (Acosta et al., 2007). Likewise, the volatility of these external capital flows can have adverse effects on the banking sector, as sudden withdrawals of savings deposits by recipient households may undermine bank liquidity and constrain the credit capacity of the financial system (Opperman & Adjasi, 2019). In addition, recipients of these funds may become excessively indebted based on the expectation of continued remittance inflows, thereby increasing banks’ exposure to potential increases in their default rates if these capital flows were to slow down or cease altogether.

Thus, while there are cases such as Mexico—where, given the importance of remittances as an income source for many households, banks have experienced increased demand for savings accounts and other financial services, leading to greater development of the banking system (Demirgüç-Kunt et al., 2011)—there are also countries where remittances and their volatility have had negative effects. These include reductions in banking efficiency due to higher net interest margins and negative impacts on financial depth, measured as the ratio of domestic credit to the private sector to GDP (Opperman & Adjasi, 2019).

Notwithstanding the extensive empirical literature, important gaps persist that this study seeks to address. First, much of the existing research adopts a cross-country or regional perspective which—although valuable for comparative purposes—may obscure the dynamics shaped by national institutions, household behavior, and the structural characteristics of each financial system. Second, country-level evidence for emerging economies such as Peru remains scarce, even though remittance inflows have become increasingly important and the Peruvian banking sector displays unique features, including regional disparities in access and persistent trust gaps in formal institutions. These gaps underscore the need for a country-focused analysis that captures the multidimensional aspects of banking development and provides lessons tailored to the Peruvian context.

Given this context, we contend that remittances positively impact the development of the Peruvian financial sector by providing an additional source of income for recipient households which, in turn, would increase the demand for financial services such as savings and credit accounts.

The main objective of this research is to estimate the causal effect of remittance inflows on the development of the Peruvian banking system. For this purpose, we analyze quarterly data from 2001 to 2024 using a two-stage least squares (2SLS) model. This model was selected to address the potential endogeneity between remittances and banking development variables. Additionally, we employ financial development indicators constructed through multidimensional indices of the banking sector using principal component analysis (PCA).

Accordingly, this study contributes to the literature in three concrete ways. First, we build a multidimensional index of banking development tailored to the Peruvian case through PCA, capturing depth, efficiency, and solvency. Second, we extend the time horizon of analysis by using quarterly data from 2001 to 2024, enabling the identification of post-pandemic dynamics and recent episodes of international volatility often absent in previous research. Third, we draw specific policy implications designed for the Peruvian context, including fiscal incentives for banks to design savings products linked to remittances, financial education programs aimed at recipient households to foster trust in formal institutions, and the promotion of digital and fintech solutions to reduce transaction costs and broaden access.

The remainder of this paper is structured as follows: Section 2 presents a theoretical framework; Section 3 reviews the literature; Section 4 describes the contextual background; Section 5 details the methodology; Section 6 presents and analyzes the data and results; and Section 7 offers conclusions and recommendations based on the findings.

2. THEORETICAL FRAMEWORK

To begin this study, it is essential to have clear definitions of remittances and financial development. The financial system, according to Bodie and Merton (2004), comprises various elements—markets, financial intermediaries, service companies, and other institutions—whose primary objective is to implement the financial decisions made by families, businesses, and governments. Among the main financial intermediaries are banks, which generate means of payment through credit, financing new investments and allowing individuals to become entrepreneurs (Schumpeter, 1911/2008).

According to post-Keynesian theory, banks—as financial intermediaries—play a crucial role in the endogenous creation of money through the banking multiplier effect (Piégay & Rochon, 2005). This theory emphasizes that the money supply cannot be controlled by the central bank but is instead determined by the demand for bank credit (Wray, 1992). The multiplier is defined as the relationship between the monetary aggregate “M” (deposits “D” and cash in the hands of the public “E”) and the monetary base “B” (bank reserves “R” and cash in the hands of the public “E”). Considering that banks maintain a minimum reserve ratio “r” imposed by the monetary authority, and that the proportion of deposits held in cash by the public is represented by “e,” the monetary multiplier is expressed as:

Thus, the multiplier increases as the reserve requirement imposed on banks decreases.

The financial system performs five main functions: it provides information about potential investments, mobilizes and aggregates savings, allocates capital, monitors investments and exercises corporate control, facilitates trade and risk management, and enables the exchange of goods and services (King & Levine, 1993).

Aligned with this perspective, Beck et al. (2000) define financial development as an increase in access to credit, with the level of inclusion as its main indicator. Levine (2005) later expanded this definition by linking financial development to improvements in the information provided by the financial system and reductions in transaction costs. From this perspective, the progressive reduction of frictions, the growing participation of clients, innovation, and financial inclusion drive the development of the financial system, facilitating intermediation between savers and investors and favoring economic growth (Kar et al., 2014).

In this sense, the efficiency and impact of the financial system on development depend on the level of financial intermediation, its efficiency, and its composition. The level of financial intermediation—which refers to the size of the financial system relative to the economy—is crucial for all financial functions. A larger financial system can reduce credit constraints, improve capital allocation, and increase responsiveness to external shocks by smoothing consumption and investment patterns (Bencivenga & Smith, 1991). Additionally, the efficiency of the financial system allows for the evaluation of its ability to allocate resources optimally, maximizing its performance while minimizing associated costs. However, factors such as asymmetric information, financial market externalities, and imperfect competition can affect efficiency and lead to inefficient capital distribution (Stiglitz & Weiss, 1981). Similarly, the composition of financial intermediation—related to the maturity of available financing and the growth of capital markets and institutional investors—also plays an important role. The maturity of loans and obligations can affect the ability to take advantage of certain investments opportunities, while the substitution of banks for markets may result from changes in intermediation costs (Jacklin, 1987).

Regarding remittances, these consist of funds transferred between households, that is, the money transfers sent by workers abroad to their home country (Organización Internacional para las Migraciones [OIM], 2020). The volume of such transfers is often related to the immigrants’ level of integration in the host country, as they usually have lower initial incomes due to lack of local skills (Malgesini & Giménez, 2000). The theories explaining the reasons for these money flows can be classified into three groups.

The first is the pure altruism model, which suggests that migrants send remittances because of their concern for the difficult economic conditions faced by their relatives in the home country (Lucas & Stark, 1985). The second is the pure selfishness model, which is based on three motives: accumulating assets in the home country, securing a larger share of family inheritance, and investing in fixed assets for an eventual return (Martínez Pizarro & Reboiras Finardi, 2001). Finally, the third model is based on the existence of an implicit contract between the migrant and their family members, in which the latter finance the expenses associated with migration, and the migrant repays this loan in the form of remittances once their financial situation improves (Cox, 1987).

Regarding the impact of remittances on development, two theories attempt to explain it: the functionalist and the historical-structuralist approaches. The functionalist theory views remittances as an injection into the circular flow of income, increasing economic activity by boosting aggregate spending. This perspective posits that remittances have the potential to reduce poverty and income inequality, and help stabilize household economies. It also highlights the presence of a multiplier effect that benefits both recipient families and the overall economy of the country (Adelman & Taylor, 1990).

On the other hand, historical-structuralist theory offers a different view, suggesting that emigration negatively impacts the economy. According to this approach, remittances create economic dependence, exacerbate social inequalities, cause inflationary effects, contribute to brain drain, and lack long-term sustainability. Furthermore, only a small portion of remittances is allocated to savings and productive investment (Toasa, 2016).

3. LITERATURE REVIEW

3.1 Remittances as a Driver of Financial Inclusion and Banking Expansion

A substantial body of literature aligns with the functionalist perspective, which emphasizes the positive role of remittances as a catalyst for financial intermediation. Giuliano and Ruiz-Arranz (2009) showed that remittance inflows stimulate deposits and credit, expanding households’ access to financial services. Aggarwal et al. (2011) similarly found that remittances enlarge the deposit base and strengthen banking efficiency, reducing transaction costs and promoting financial depth, particularly in countries with greater government involvement in banking. In Mexico, Demirgüç-Kunt et al. (2011) observed that remittances increased both the breadth and depth of the banking system, consistent with the post-Keynesian view that deposit growth supports endogenous credit creation.

Other studies emphasize the role of remittances in promoting financial inclusion. Anzoategui et al. (2014) highlighted that remittance inflows encourage households to interact more actively with banks, allowing recipients to secure these funds, smooth their consumption, and use them as collateral when applying for credit. Remittances also help reduce knowledge barriers by increasing households’ interaction with financial institutions (Ajefu & Ogebe, 2019). In Asia, Akçay (2019) concluded that remittances in Bangladesh enabled the integration of previously unbanked households, while Haruna (2019) demonstrated that in supportive policy environments, remittances shield households from weak intermediation.

Cross-regional studies further confirm these findings. Gupta et al. (2009), analyzing Sub-Saharan Africa, observed that despite the region receives a relatively small share of global remittances, these flows contributed positively to financial development through greater inclusion. Toxopeus and Lensink (2007) reported a significantly positive impact of remittances on financial development across developing economies, while Ramirez and Sharma (2008) suggested that remittances and financial development may function as substitutes for growth, given their capacity to ease credit constraints. In Europe, Male (2009) identified a strong positive association between remittances and financial sector development under a fixed-effects framework, while Esteves and Khoudour-Castéras (2011), using pooled ordinary least squares (OLS) for 1870-1913, concluded that remittances reinforced the expansion of financial systems.

Longitudinal analyses further deepen these insights. Ajilore and Ikhide (2012) found that remittances were a central driver of financial development from 1985 to 2009, exerting effects in both the short and long run. In contrast, Karikari et al. (2016) argued that while remittances positively influence financial development in the short term, such effects are not always sustained in the long term.

Within Latin America, further evidence supports these conclusions. Fajnzylber and Lopez (2008), using household survey data, found that remittances were associated with higher ownership of bank accounts in El Salvador and Mexico, although the effect was more limited in countries with weaker financial institutions. Similarly, Orozco and Fedewa (2006) observed that remittance recipients across Central America were more likely to open deposit accounts, thereby expanding financial inclusion. More recently, Fromentin (2018), analyzing 39 Latin American and Caribbean countries, found a bidirectional positive relationship, suggesting that stronger financial systems magnify the developmental role of remittances.

The most recent contributions consolidate these findings. Forhad et al. (2023) demonstrated that transfers from less-skilled migrants particularly enhance financial inclusion, underscoring the heterogeneity of impacts across households. Prempeh et al. (2023) established a long-term cointegration between remittances and financial development in Ghana, highlighting complementarity rather than substitution. Islam and Mondal (2023) confirmed these findings in Latin America, showing that remittances strengthen financial development over the long run. These results consistently reflect the functionalist argument that remittances serve as an injection of liquidity that broadens the reach of financial systems.

3.2 Risks, Volatility, and Institutional Constraints

In contrast to functionalist arguments, the structuralist perspective emphasizes that remittances may generate dependency and instability rather than sustained financial deepening. Brown et al. (2013) argued that remittance inflows can discourage borrowing, thereby reducing incentives for financial intermediation. Consistently, Ambrosius and Cuecuecha (2016) found that remittances can substitute for credit by alleviating liquidity constraints, thereby weakening demand for loans. These findings resonate with Stiglitz and Weiss’s (1981) argument that reduced credit demand can undermine the efficiency of financial allocation.

The volatility of remittances has also been identified as a systemic risk for banking systems. Opperman and Adjasi (2019) demonstrated that irregular inflows undermine bank liquidity, as sudden deposit withdrawals can force institutions to increase transfer costs, thereby reducing efficiency and stability. Adekunle et al. (2020) similarly argued that although remittances may temporarily ease financial constraints, they can reduce the incentive to borrow, resulting in stagnation in the loan market and weakening the long-term dynamics of financial intermediation. Furthermore, institutional weaknesses exacerbate these risks: Coulibaly (2015) highlighted that fragile governance structures in Sub-Saharan Africa constrained the potential benefits of remittances, limiting their contribution to banking development.

Evidence from Latin America echoes these concerns. Fajnzylber and Lopez (2008) observed that recurrent financial crises in the region eroded households’ trust in banks, thereby curtailing the positive spillovers of remittance inflows. In a similar vein, Ikpesu et al. (2020) showed that institutional quality is decisive in determining whether remittances enhance or undermine banking systems, underscoring the structuralist claim that remittances alone cannot compensate for institutional fragility.

Recent research provides further support for these arguments by focusing on external shocks and governance conditions. Bansak et al. (2025) examined the U.S. COVID-19 response and showed how labor-market shocks in sending countries directly disrupt remittance flows, reinforcing the structuralist claim that these inflows are highly volatile. Barkat et al. (2024) studied remittances and the Sustainable Development Goals, concluding that while remittances can promote inclusive growth, their developmental role depends on strong institutional and governance frameworks. Nawshin et al. (2024) further demonstrated that in Bangladesh, remittances reduce external debt pressures and bolster reserves, but only under favorable macroeconomic conditions. Taken together, these findings highlight the institutional and macroeconomic constraints that limit the transformative potential of remittances, showing that without strong governance and stability, remittances may exacerbate financial fragility.

3.3 Methodological Advances and Multidimensional Approaches

A third strand of the literature emphasizes the methodological challenges of measuring financial development and its link to remittances. Early contributions relied on narrow proxies—typically credit-to-GDP ratios—which provided only partial insights into the complex dynamics of financial systems. Similarly, Esteves and Khoudour-Castéras (2011), drawing on European data from 1870 to 1913, and Male (2009), using fixed-effects estimations for European countries, confirmed the positive influence of remittances but were constrained by single-dimensional indicators. These limitations echo the concerns raised by Beck et al. (2010), who argued that financial development should be assessed through multiple channels, including depth, access, and efficiency.

Building on this theoretical imperative, Jolliffe (2002) introduced PCA as a statistical method to build composite indices from multiple variables. In line with this, Sahay et al. (2015) developed the International Monetary Fund’s (IMF) financial development index, which operationalizes a multidimensional approach that assesses access, efficiency, and depth in a consolidated framework.

Recent contributions extend this line of research. Bilalli and Sadiku (2023) showed how inflation interacts with banking sector stability, illustrating that macroeconomic shocks can offset the gains from remittances and therefore highlighting the importance of including solvency and efficiency dimensions in composite indices. Weerawarna and Miah (2023) also underscored how digital rails (e.g., blockchain) and predictive analytics can reduce costs and enhance operational efficiency in remittance intermediation, further justifying measurement frameworks that go beyond transaction volumes to capture quality and resilience.

By incorporating these multidimensional approaches, scholars move closer to the post-Keynesian view that financial development must be assessed not only by volume but also by efficiency, stability, and institutional resilience. This methodological evolution supports the present study’s use of a PCA-based composite index to capture the complex interaction between remittances and the Peruvian banking sector.

4. BACKGROUND: THE CASE OF PERU

International migration has increased due to economic, demographic, political, and social factors that have led many Peruvians to seek better living conditions abroad. In the past three decades, this flow has intensified, with labor-related reasons as the main driver (International Organization for Migration & Instituto Nacional de Estadística e Informática, 2015)..

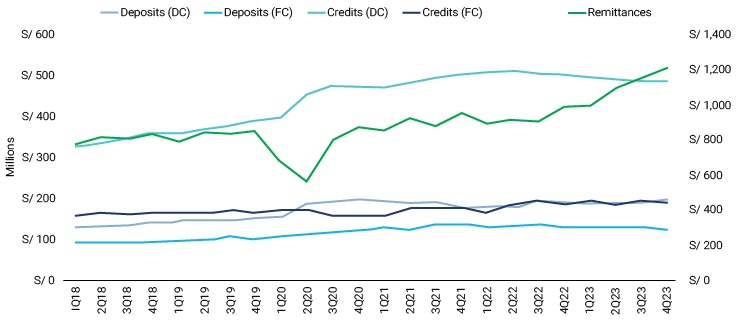

During the last five years, Peru has received an annual average of USD 3,2 billion in remittances sent to Peruvian families by household members residing abroad (INEI, 2022). In the most recent year, remittance inflows reached USD 4446 million, representing a 19,9 % increase compared to the previous year and accounting for 2 % of the GDP. This growth is primarily driven by the recovery of employment in the United States—the main source of remittances to Peru—followed by Spain, Italy, Chile, and Argentina (BCRP, 2023). Figure 1 complements these annual figures by showing the quarterly evolution, in soles, of remittances together with deposits and bank credit; therefore, the figure should be read as a trend comparison rathen than as the direct source of the dollar and percentage figures reported above.

Figure 1

Remittances, Deposits, and Bank Credits

Note. Left y-axis: deposits and credits in domestic currency (DC) and foreign currency FC expressed in millions of soles. Right y-axis: remittances, expressed in millions of soles. Adapted from Memoria 2023, by BCRP, 2023 (https://www.bcrp.gob.pe/publicaciones/memoria-anual/memoria-2023.html).

Regarding remittance transfer modalities, a reduction has been observed in the use of informal channels, alongside an increase in the use of empresas de transferencia de fondos (ETF – money transfer operators) and banks, which in 2023 accounted for 4 %, 53,9 %, and 42,1 % of total remittances, respectively (BCRP, 2023). This decrease in the use of informal channels has been promoted by initiatives such as the “Mobilization of Remittances through Microfinance Institutions” project led by the Módulo de Instrumentos Financieros (MIF – Financial Instrument Module), which encourages the use of remittances through the formal financial system (OIM & INEI, 2015).

With respect to the financial system, Peru’s landscape is mostly made up of savings and credit cooperatives, although private banks hold the majority of assets. Currently, the system comprises 17 multiple-service banking institutions and two state-owned banks. However, the four largest banks—Banco de Crédito del Perú (BCP), BBVA, Scotiabank, and Interbank) account for 81,3 % of the direct credits in the banking system (Apoyo & Asociados Internacionales S. A. C., 2022).

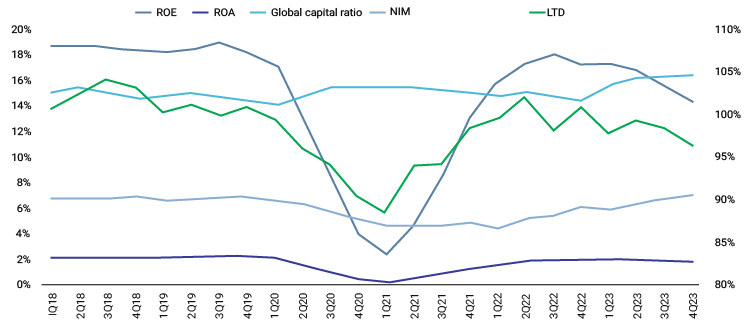

In terms of solvency, the financial system has remained stable in recent

years, with a global capital ratio of 16,47 % in the last quarter of 2023—above the regulatory minimum of 9 % established by the Superintendencia de Banca, Seguros y AFP (SBS). Profitability, measured by return on equity (ROE), has recovered since the COVID-19 pandemic, reaching 14,29 %, while return on assets (ROA) was 1,81 %. The net interest margin (NIM) has exceeded pre-pandemic levels, reaching 6,97 %. In terms of liquidity, the loan-to-deposit (LTD) ratio stands at 96,37 %, indicating high use of deposits to grant loans, which increases profitability but also liquidity risk. Regarding financial inclusion, significant progress has been observed in the region, with inclusion levels increasing from 37,9 % in 2021 to 43,3 % in 2023 (Observatorio Económico, Financiero y Social, 2024). Figure 2 summarizes the recent quarterly evolution of these banking indicators, distinguishing the series reported on the left and right y-axes.

Figure 2

Banking System Indicators

Note. Left y-axis: ROE, ROA, global capital ratio and net interest margin (NIM). Right y-axis: loan-on-deposit ratio (LTD). All series expressed as percentages. Adapted from Reporte trimestral del sistema financiero: Marzo 2024, by Observatorio Económico, Financiero y Social, 2024 (https://www.ulima.edu.pe/sites/default/files/page/file/reporte_trimestral_sistema_financiero_marzo_2024.pdf).

5. METHODOLOGY

Measuring banking sector development poses an inherent methodological challenge. Traditional approaches often rely on single proxies—such as the ratio of deposits or loans to GDP (Aggarwal et al., 2011; Giuliano & Ruiz-Arranz, 2009)—or on breadth indicators such as the number of bank branches or deposit accounts per capita (Demirgüç-Kunt et al., 2011). While these indicators provide useful insights, they present important limitations: a system with wide outreach may still be fragile, and one with high intermediation levels may allocate resources inefficiently or concentrate credit among the hands of a small number of borrowers, leading to distortions (Bettin & Zazzaro, 2012). As Haruna (2019) emphasizes, relying solely on depth or breadth overlooks the fact that a larger or more extensive banking sector is not necessarily efficient or stable.

In light of these limitations, this study adopts a multidimensional approach to banking sector development. Instead of relying on a single metric, a composite index that combines different aspects of the financial system is constructed, allowing for a joint assessment of both the scale, quality, and resilience of the sector. Specifically, the index includes: (i) loans and deposits of the banking system as indicators of intermediation depth; (ii) the net interest margin as a measure of efficiency; and (iii) the ratio of liabilities to equity and reserves as a proxy for solvency. In this way, the index simultaneously reflects the intermediation capacity, profitability, and soundness of financial institutions.

A central aspect of constructing this index is the assignment of weights to each dimension. Equal weighting assumes identical contributions across all indicators, which rarely corresponds to empirical reality. Conversely, expert-based weighting introduces subjectivity. To overcome this problem, PCA is employed, allowing weights to be determined endogenously based on the statistical structure of the data (Jolliffe, 2002; Saisana & Tarantola, 2002).

PCA is a statistical technique that reduces the dimensionality of a dataset while preserving as much variability as possible. It transforms the original data into a new set of uncorrelated variables called principal components, ordered such that the first component captures the largest share of total variability, the second explains the largest share of the remaining variability not captured by the first, and so on. This technique is especially useful in the analysis of large datasets with many interrelated variables, as it facilitates the visualization, processing, and interpretation of the data (Jolliffe, 2002).

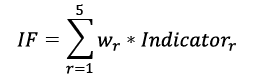

The composite index is calculated as follows:

where wr represents the factor loadings extracted from the first principal component and r corresponds to the four measures of banking sector development. In this way, the weights reflect the relative importance of each indicator within the common structure of the data.

Subsequently, the indicator is normalized on a 0–1 scale to facilitate better analysis. The normalization formula is:

This transformation facilitates the interaction of the index in relative terms and ensures comparability over time. By combining a PCA-based weighting scheme with normalization, the index provides a robust, coherent, and methodologically consistent measure of banking sector development.

On the other hand, to estimate the empirical model, this study applies the 2SLS method. Standard linear regression models assume that the errors of the dependent variable are not correlated with the independent variables. However, when such correlation exists, the OLS method does not provide optimal estimates. Instead, the 2SLS method extends the standard framework by addressing the endogeneity problem that could bias the results, using instrumental variables uncorrelated with the error term.

Because one of the necessary conditions for two-stage regression models is the exogeneity of the explanatory variables—i.e., that they are not correlated with the error term—the endogeneity test was performed using the Durbin-Wu-Hausman (DWH) test. The DWH test evaluates whether endogeneity is present among the explanatory variables of the model. If the test indicates that the standard OLS estimators are inconsistent due to autocorrelation in the errors, this suggests that the explanatory variables might be endogenous. In such a case, the use of instrumental variables through a 2SLS model is warranted to obtain consistent and valid estimates (Greene, 2002).

The 2SLS model is a technique used to solve endogeneity problems in linear regression models. Endogeneity occurs when one or more explanatory variables are correlated with the error term, which can lead to biased and inconsistent estimates. The 2SLS approach addresses this problem by using instruments that are correlated with the endogenous variables but uncorrelated with the error term.

The 2SLS methodology is developed in two phases. In the first phase, instrumental variables that are uncorrelated with the error are used to estimate the endogenous

variables.

where bst is the dependent variable, remitt is the endogenous variable invt, cpit fdit,gdpt, tradet, and instt are the control variables; and ηt is the error term

Estimation of the endogenous variable:

where, remitt−1 is the lag of remittances, bst−1 is the lag of the banking sector, α0, α1, α2, and β1, β2, . . . , β6, are the coefficients to be estimated, and εt is the error term in this first stage.

Fitted values of remitt :

These fitted values of  are the predictions obtained from the regression of remittances on the instruments.

are the predictions obtained from the regression of remittances on the instruments.

In the second phase, the predicted values of the endogenous variables are incorporated into the main regression to estimate the effect on the dependent variable, ensuring that the estimates are consistent and unbiased.

Since the instrument selection is not arbitrary—requiring that both the relevance and exogeneity conditions be met—the Sargan (1958) and Basmann (1960) constraint overidentification tests are used to evaluate the validity of the instruments. Additionally, a weak-instrument test is carried out to measure the strength of the instruments and verify if they are appropriate to correct for endogeneity.

DATABASE

This study focused on Peru and analyzed quarterly data from January 2001 to March 2024. The variables analyzed included foreign remittances, banking development, inflation rate, economic growth, investment, financial openness, and economic openness.

First, foreign remittance data were obtained from the BCRP database. Second, the variables needed to construct the banking development index were collected from the SBS on a monthly basis and subsequently adjusted to a quarterly frequency. Third, inflation was measured using the consumer price index (CPI), with data obtained from the BCRP. Fourth, GDP data—also provided by the BCRP—were used at constant 2018 prices in millions of dollars. Economic growth was calculated as the annual growth rate of total GDP after applying logarithmic transformations.

Investment was assessed by gross fixed capital formation as a percentage of GDP, using BCRP data. Financial openness was measured using foreign direct investment (FDI) as a percentage of GDP, also provided by the BCRP. Finally, economic openness was calculated as the sum of total exports and imports as a percentage of GDP, according to BCRP data.

6. RESULTS

Justification of the Model

DWH Test

As shown in the figure, the p-values lead us to reject the null hypothesis (H0), which assumes that OLS estimators remain valid even with autocorrelation. Therefore, we accept the alternative hypothesis (Ha), which suggests that autocorrelation compromises the validity of OLS estimators, making them biased and inefficient. This justifies the use of instrumental variables.

Table 1

DWH Test

|

estat endog |

||||

|

Tests of endogeneity |

||||

|

H0: Variables are exogenous |

||||

|

Durbin (score) χ2 (1) |

= 8,3677 (p = 0,0038) |

|||

|

Wu-Hausman F (1,82) |

= 8,3036 (p = 0,0050) |

|||

Note. estat endog = endogeneity statistic; H₀ = null hypothesis; χ² = chi-square distribution.

Instrument Selection

Overidentification Test

The validity of the instruments in our model was evaluated using the Sargan and Basmann constraint overidentification tests, which assess whether the additional instruments are exogenous and uncorrelated with the error term.

The Sargan test yielded a chi-square statistic of 2,93319 (p = 0,0868), while the Basmann test produced a statistic of 2,73112 (p = 0.0984). Because both p-values exceed the 0,05 threshold, the null hypothesis of instrument validity cannot be rejected. These results evidence that the selected instruments are not correlated with the error term, supporting the consistency and robustness of the model estimates.

Relevance Test (F-Test)

Recognizing that instrument relevance is a necessary condition for choosing a valid instrument for our model, we conducted an F-test in the first stage to verify if the instruments were correlated with the endogenous variable. The results were favorable: the F value of the test as a whole reached a value of 50,3627—well above 10—which suggests that the instruments were relevant.

2SLS Model

Table 2 shows that remittances have a significant impact on the development of the banking sector. An increase of one million dollars in remittances from abroad generatesan increase of 0.13 units in the banking sector development index. This impact is particularly reflected in the growth of deposits and loans. Orozco and Fedewa (2006) point out that remittances, by increasing disposable income and boosting confidence in the banking sector, encourage families to deposit their funds instead of keeping them in cash. In addition, this increase in resources may expand credit availability, facilitating access to financing for both individuals and businesses (Giuliano & Ruiz-Arranz, 2009).

A greater volume of deposits strengthens the available capital of banks, improving their capacity to absorb losses and, consequently, their solvency. Aggarwal et al. (2011) found that remittances—coming from sources outside the local market—serve as a buffer against domestic economic shocks, thus contributing to banks’ financial stability. Finally, as deposits rise and lending capacity expands, banks can increase their interest and fee income, optimize resource allocation, and reduce operating costs, thus improving their financial margins (Birchwood et al., 2017).

FDI also has a positive impact on the banking sector development by facilitating the expansion of financial services and the adoption of advanced technologies, which improve operational efficiency and security (Claessens et al., 2001). Likewise, the presence of foreign financial institutions can increase confidence in the local financial system and attract more investment, strengthening financial stability (Goldberg, 2007).

In relation to gross fixed capital formation (GFCF), its positive and significant impact on the development of the banking sector stands out, since an increase of USD 1 million in GFCF raises the banking sector indicator by 0,17. Because GFCF typically requires financing, it increases the demand for credit. Both firms and governments that invest in fixed capital often need loans to finance their projects, which intensifies banking activity (Al-Zubi et al., 2006). Moreover, as the productive capacity of the economy expands, higher income and savings are generated, which in turn can be channeled into the banking system, thus enlarging its deposit base and lending capacity (Mhadhbi et al., 2020).

In addition, inflation also has a significant impact on the development of the banking sector: a 1 % increase in the inflation rate decreases the banking development indicator by 0,15. High inflation can reduce the value of financial assets and deposits, generating uncertainty and reducing confidence in the banking system. Faced with higher credit risks and interest-rate fluctuations, banks may adopt more restrictive lending policies (Boyd & Champ, 2009). Inflation can also negatively affect savings rates, decreasing the resources available for lending. In extreme situations, uncontrolled inflation can lead to a banking crisis, where financial institutions struggle to maintain stability and solvency (Bilalli & Sadiku, 2023).

Likewise, GDP has a positive and significant impact on the development of the banking sector. GDP growth reflects an expanding economy that generally increases savings and the demand for financial services. Levine (1997) and Sahay et al. (2015) argue that economic growth and financial development are interrelated, as a growing economy generates more income and savings, providing additional resources to the banking system and promoting economic development through the financing of business and infrastructure projects. Arcand et al. (2015) further show that financial development, enhanced by GDP growth, can have a positive effect on macroeconomic stability by diversifying financing sources and reducing vulnerability to external shocks.

Next, we find that trade openness has a positive impact on the banking system.This occurs because, when foreign trade increases, firms need more banking services to handle international transactions. Rajan and Zingales (2003) argue that trade openness contributes to international financial integration by fostering competition and encouraging the adoption of better banking practices. Furthermore, Baltagi et al. (2009) suggest that trade liberalization can enhance banking efficiency by allowing foreign banks to enter the market, as they often introduce new technologies and better risk management practices. In turn, Do and Levchenko (2004) find that foreign trade can foster the development of the banking system by increasing liquidity and diversifying banks’ sources of income, thus improving their resilience to economic fluctuations.

Finally, regarding institutional framework, a positive and significant impact on the development of the banking sector is observed. This is because a robust institutional environment fosters the stability and efficiency of the financial system, as sound and well-regulated institutions promote investor and depositor confidence, thus facilitating financial intermediation and access to credit. A recent study by Beck et al. (2010) confirms that institutional quality is a key determinant of financial development. This study shows that countries with better institutions tend to have more developed and efficient banking systems. Furthermore, Nissanke and Stein (2003) emphasize that the transformation of the financial system is primarily an institutional transformation, indicating that financial development not only depends on market liberalization or financial innovation but also requires a sound institutional infrastructure to support the smooth functioning of the system.

Table 2 reports the 2SLS estimation results for the model.

Table 2

2SLS Summary Statistics

|

Instrumental Variables 2SLS Regression |

Number of observations = 91 |

|||||

|

Wald χ²(7) = 3975,27 |

||||||

|

Probability > χ² = 0,0000 |

||||||

|

R-squared = 0,9776 |

||||||

|

Root MSE = 0,0508 |

||||||

|

bs |

Coefficient |

Standard Error |

z |

P > | z | |

[95 % Confidence interval] |

|

|

remit |

0,1274 |

0,0531 |

2,40 |

0,016 |

0,2315 |

0,0233 |

|

inv |

0,0165 |

0,0074 |

2,23 |

0,026 |

0,0310 |

0,0020 |

|

cpi |

-0,0149 |

0,0027 |

-5,44 |

0,000 |

-0,0095 |

-0,0202 |

|

fdi |

0,0000 |

5,43e-06 |

2,47 |

0,014 |

0,0000 |

2,75e-06 |

|

gdp |

1,65e-06 |

7,31e-07 |

2,26 |

0,024 |

2,21e-07 |

3,09e-06 |

|

trade |

0,0049 |

0,1634 |

0,03 |

0,036 |

0,2153 |

0,3251 |

|

inst |

0,0006 |

0,0042 |

0,15 |

0,049 |

0,0086 |

0,0076 |

|

_cons |

-0,6781 |

0,3201 |

-2,12 |

0,034 |

-1,3055 |

-0,0508 |

|

Instrumented: |

remit |

|||||

|

Instruments: |

inv, cpi, fdi, gdp, trade, inst, rezrem, rezb |

|||||

Note. bs = banking sector; remit = remittances; inv = investment; cpi = consumer price index; fdi = foreign direct investment; gdp = gross domestic product; trade = trade openness; inst = institutional quality; _cons = constant; rezrem = lagged remittances; rezb = lagged banking sector development index.

7. CONCLUSIONS

This study provides new evidence on the role of remittances in shaping banking sector development in Peru during the period 2001–2024, using a 2SLS estimation framework. The results confirm that remittance inflows exert a positive and significant impact on the financial system. This effect is most visible in the growth of deposits and loans, because as households gain confidence in banks, they increasingly deposit funds that would otherwise remain in cash holdings. The additional resources strengthen banks’ capital base, enhancing their ability to absorb potential losses and improving their solvency. At the same time, greater deposit mobilization allows banks to expand credit supply, thereby facilitating access to financing for both households and firms. The expansion of the loan portfolio not only fosters economic activity but also contributes to the diversification of credit risk. Moreover, higher deposit volumes and increased lending capacity translate into stronger revenues from interest and fees, more efficient allocation of resources, and lower operational costs, which together reinforce banks’ financial margins and overall stability. The analysis further reveals that other macroeconomic and institutional factors also condition banking development. Foreign direct investment and gross fixed capital formation act as positive drivers by expanding financial services, enhancing operational efficiency, and supporting greater credit capacity. By contrast, inflation exerts a destabilizing effect, undermining financial soundness. Meanwhile, GDP growth and trade openness stimulate banking deepening by raising credit demand, expanding the scope of financial intermediation, and fostering competition within the sector.

Taken together, these findings underscore that remittances are not merely a private household resource but a macro-financial flow with the potential to strengthen intermediation and improve banking resilience. However, the developmental impact of these flows is not automatic; it depends critically on the institutional and policy environment. Strengthening this channel requires measures that integrate remittances more directly into the formal financial system. One avenue is the design of fiscal incentives that encourage banks to develop savings and investment products tailored to remittance recipients, thereby channeling funds toward productive uses. At the same time, targeted financial literacy programs can increase households’ willingness to use formal institutions, reduce reliance on informal saving mechanisms, and ultimately foster inclusion. A further policy priority is the promotion of digital platforms and Fintech innovations, which can reduce transaction costs, expand outreach in underserved areas, and accelerate the integration of remittances into the banking sector. Moreover, coordinated action between regulators and financial institutions is essential to direct remittance-linked deposits toward small and medium-sized enterprises (SMEs) and infrastructure investment—sectors that generate broad-based economic growth.

Finally, the study opens relevant avenues for future research. Regional heterogeneities within Peru remain largely unexplored, despite the marked differences in remittance use and financial inclusion between urban and rural areas. Furthermore, the rapid expansion of digital remittances and Fintech solutions warrants systematic research, particularly regarding their potential to reshape intermediation, improve resilience, and influence household investment behavior. Exploring these dimensions would not only complement the present findings but also contribute to a more nuanced understanding of the broader role of remittances in financial development.

REFERENCES

Acosta, P. A., Fajnzylber, P., & Lopez, J. H. (2007). The impact of remittances on poverty and human capital: Evidence from Latin American household surveys (Policy, Research Working Paper No. 4247). World Bank. https://documents.worldbank.org/en/publication/documents-reports/documentdetail/446091468046772511

Adekunle, I. A., Williams, T. O., Omokanmi, O. J., & Onayemi, S. O. (2020). Mediating roles of institutions in the remittance-growth relationship: Evidence from Nigeria (AGDI Working Paper No. WP/20/063). African Governance and Development Institute. https://www.econstor.eu/bitstream/10419/228040/1/1731778201.pdf

Adelman, I., & Taylor, J. E. (1990). Is structural adjustment with a human face possible: The case of Mexico. The Journal of Development Studies, 26(3), 387-407. https://doi.org/10.1080/00220389008422161

Aggarwal, R., Demirgüç-Kunt, A., & Martínez Pería, M. S. (2011). Do remittances promote financial development? Journal of Development Economics, 96(2), 255-264. https://doi.org/10.1016/j.jdeveco.2010.10.005

Ajefu, J. B., & Ogebe, J. O. (2019). Migrant remittances and financial inclusion among households in Nigeria. Oxford Development Studies, 47(3), 319-335. https://doi.org/10.1080/13600818.2019.1575349

Ajilorea, T., & Ikhider, S. (2012). A bounds testing analysis of migrants remittances and financial development in selected Sub-Sahara African countries. The Review of Finance & Banking, 4(2), 79-96. https://www.ceeol.com/search/article-detail?id=848701

Akçay, S. (2019). Remittances and financial development in Bangladesh: Substitutes or complements? Applied Economics Letters, 27(14), 1206-1214. https://doi.org/10.1080/13504851.2019.1676376

Al-Zubi, K. M., Al-Rjoub, S. A. M., & Abu-Mhareb, E. (2006). Financial development and economic growth: A new empirical evidence from the MENA countries, 1989-2001. Applied Econometrics and International Development, 6(3). https://ssrn.com/abstract=1247522

Ambrosius, C., & Cuecuecha, A. (2016). Remittances and the use of formal and informal financial services. World Development, 77, 80-98. https://doi.org/10.1016/j.worlddev.2015.08.010

Anzoategui, D., Demirgüç-Kunt, A., & Martínez Pería, M. S. (2014). Remittances and financial inclusion: Evidence from El Salvador. World Development, 54, 338-349. https://doi.org/10.1016/j.worlddev.2013.10.006

Apoyo & Asociados Internacionales S. A. C. (2022). Sistema bancario peruano 2022: reporte sectorial. https://www.aai.com.pe/wp-content/uploads/2023/04/Sistema-Bancario-Peru%CC%81-2022.pdf

Arcand, J. L., Berkes, E., & Panizza, U. (2015). Too much finance? Journal of Economic Growth, 20, 105-148. https://doi.org/10.1007/s10887-015-9115-2

Baltagi, B. H., Demetriades, P. O., & Law, S. H. (2009). Financial development and openness: Evidence from panel data. Journal of Development Economics, 89(2), 285-296. https://doi.org/10.1016/j.jdeveco.2008.06.006

Banco Central de Reserva del Perú. (2023). Memoria 2023. https://www.bcrp.gob.pe/publicaciones/memoria-anual/memoria-2023.html

Banco Central de Reserva del Perú. (2024, February 27). Remesas del exterior crecieron 19,9% en 2023. https://www.bcrp.gob.pe/docs/Transparencia/Notas-Informativas/2024/nota-informativa-2024-02-27.pdf

Bansak, C., Glebocki, H., & Simpson, N. B. (2025). The impact of the U.S. Covid-19 response on remittance flows to emerging markets and developing economies. International Economics, 182, Article 100580. https://doi.org/10.1016/j.inteco.2025.100580

Barkat, K., Mimouni, K., Alsamara, M., & Mrabet, Z. (2024). Achieving the sustainable development goals in developing countries: The role of remittances and the mediating effect of financial inclusion. International Review of Economics & Finance, 95, Article 103460. https://doi.org/10.1016/j.iref.2024.103460

Basmann, R. L. (1960). On finite sample distributions of generalized classical linear identifiability test statistics. Journal of the American Statistical Association, 55(292), 650-659. https://doi.org/10.1080/01621459.1960.10483365

Beck, T., Demirgüç-Kunt, A., & Levine, R. (2010). Financial institutions and markets across countries and over time: The updated financial development and structure database. The World Bank Economic Review, 24(1), 77-92. https://doi.org/10.1093/wber/lhp016

Beck, T., Levine, R., & Loayza, N. (2000). Finance and the sources of growth. Journal of Financial Economics, 58(1-2), 261-300. https://doi.org/10.1016/S0304-405X(00)00072-6

Bencivenga, V. R., & Smith, B. D. (1991). Financial intermediation and endogenous growth. The Review of Economic Studies, 58(2), 195–209. https://doi.org/10.2307/2297964

Bettin, G., & Zazzaro, A. (2012). Remittances and financial development: Substitutes or complements in economic growth? Bulletin of Economic Research, 64(4), 509-536. https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1467-8586.2011.00398.x

Bilalli, A., & Sadiku, M. (2023). The impact of inflation on financial sector performance: Evidence. From. Western Balkan countries. SEEU Review, 18(2), 74-89. http://dx.doi.org/10.2478/seeur-2023-0071

Birchwood, A., Brei, M., & Noel, D. M. (2017). Interest margins and bank regulation in Central America and the Caribbean. Journal of Banking & Finance, 85, 56-68. https://doi.org/10.1016/j.jbankfin.2017.08.003

Bodie, Z., & Merton, R. C. (2004). Finanzas (F. Reyes Guerrero, Trans). Pearson Educación.

Boyd, J., & Champ, B. (2009). Inflation and financial market performance: What have we learned in the last ten years? In D. E. Altig & E. Nosal (Eds.), Monetary policy in low-inflation economies (pp. 259-301). Cambridge University Press. https://doi.org/10.1017/CBO9780511605475

Brown, R. P. C., Carmignani, F., & Fayad, G. (2013). Migrants’ remittances and financial development: Macro- and micro-level evidence of a perverse relationship. The World Economy, 36(5), 636-660. https://doi.org/10.1111/twec.12016

Claessens, S., Demirgüç-Kunt, A., & Huizinga, H. (2001). How does foreign bank entry affect domestic banking markets? Journal of Banking & Finance, 25(5), 891-911. https://doi.org/10.1016/S0378-4266(00)00102-3

Coulibaly, D. (2015). Remittances and financial development in Sub-Saharan African countries: A system approach. Economic Modelling, 45, 249-258. https://doi.org/10.1016/j.econmod.2014.12.005

Cox, D. (1987). Motives for private income transfers. Journal of Political Economy, 95(3), 508-546. https://doi.org/10.1086/261470

Demirgüç-Kunt, A., López Córdova, E., Martínez Pería, M. S., & Woodruff, C. (2011). Remittances and banking sector breadth and depth: Evidence from Mexico. Journal of Development Economics, 95(2), 229-241. https://doi.org/10.1016/j.jdeveco.2010.04.002

Do, Q.-T., & Levchenko, A. A. (2004, June 17). Trade and financial development (SSRN Working Paper No. 610391). SSRN. https://ssrn.com/abstract=610391

Esteves, R., & Khoudour-Castéras, D. (2011). Remittances, capital flows and financial development during the mass migration period, 1870-1913. European Review of Economic History, 15(3), 443-474. https://doi.org/10.1017/S1361491611000037

Fajnzylber, P., & Lopez, J. H. (Eds.). (2008). Remittances and development: Lessons from Latin America. World Bank. https://hdl.handle.net/10986/6911

Forhad, M. A. R., Alam, G. M., & Rahman, M. T. (2023). Effect of remittance-sending countries’ type on financial development in recipient countries: Can the pandemic make a difference? Journal of Risk and Financial Management, 16(4), Article 229. https://doi.org/10.3390/jrfm16040229

Fromentin, V. (2018). Remittances and financial development in Latin America and the Caribbean countries: A dynamic approach. Review of Development Economics, 22(2), 808-826. https://doi.org/10.1111/rode.12368

Giuliano, P., & Ruiz-Arranz, M. (2009). Remittances, financial development, and growth. Journal of Development Economics, 90(1), 144-152. https://doi.org/10.1016/j.jdeveco.2008.10.005

Goldberg, L. S. (2007). Financial sector FDI and host countries: New and old lessons. Economic Policy Review, 13(1), 1-17. https://ideas.repec.org/a/fip/fednep/y2007imarp1-17nv.13no.1.html

Greene, W. H. (2002). Econometric analysis (5th ed.). Prentice Hall. https://www.ctanujit.org/uploads/2/5/3/9/25393293/_econometric_analysis_by_greence.pdf

Gupta, S., Pattillo, C. A., & Wagh, S. (2009). Effect of remittances on poverty and financial development in Sub-Saharan Africa. World Development, 37(1), 104-115. https://doi.org/10.1016/j.worlddev.2008.05.007

Haruna, I. (2019). Harnessing international remittances for financial development: The role of monetary policy. Ghana Journal of Development Studies, 16(2), 113-137. https://mpra.ub.uni-muenchen.de/97004/

Ikpesu, F., Akinola, A., & Ikpesu, O. A. (2020). Remittance flows and banking sector development in emerging markets: Do institutions matter? Journal of Transnational Management, 27(2), 85-96. https://doi.org/10.1080/15475778.2020.1788916

Instituto Nacional de Estadística e Informática. (2022, February 19). Remesas alcanzan más de US$ 3 500 millones y crecen 22%, recuperando niveles prepandemia [Press release]. https://m.inei.gob.pe/prensa/noticias/remesas-alcanzan-mas-de-us-3-500-millones-y-crecen-22-recuperando-niveles-prepandemia-13440/

Islam, S. B., & Mondal, L. (2023). An empirical analysis on remittances and financial development in Latin American countries. Arxiv. https://arxiv.org/abs/2309.08855

Jacklin, C. J. (1987). Demand deposits, trading restrictions, and risk sharing. In E. C. Prescott & N. Wallace (Eds.), Contractual arrangements for intertemporal trade (pp. 26-47). University of Minnesota Press. https://safe-frankfurt.de/fileadmin/user_upload/editor_common/Visitors_Center/2_Jacklin_DemandDeposits.pdf

Jolliffe, I. T. (2002). Principal component analysis (2nd ed.). Springer. https://doi.org/10.1007/b98835

Kar, M., Nazlioglu, S., & Agir, H. (2014). Trade openness, financial development and economic growth in Turkey: Linear and nonlinear causality analysis. Journal of BRSA Banking and Financial Markets, 8(1), 63-86.

Karikari, N. K., Mensah, S., & Harvey, S. K. (2016). Do remittances promote financial development in Africa? SpringerPlus, 5, Article 1011. https://doi.org/10.1186/s40064-016-2658-7

King, R. G., & Levine, R. (1993). Finance, entrepreneurship and growth. Journal of Monetary Economics, 32(3), 513-542. https://doi.org/10.1016/0304-3932(93)90028-E

Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35(2), 688-726. https://ideas.repec.org/a/aea/jeclit/v35y1997i2p688-726.html

Levine, R. (2005). Finance and growth: Theory and evidence. In P. Aghion & S. N. Durlauf (Eds.), Handbook of Economic Growth (Vol. 1, Pt. A, pp. 865-934). Elsevier. https://doi.org/10.1016/S1574-0684(05)01012-9

Lucas, R. E. B., & Stark, O. (1985). Motivations to remit: Evidence from Botswana. Journal of Political Economy, 93(5), 901-918. https://doi.org/10.1086/261341

Male, S. (2009). Remittances and financial development: A study of the South-Eastern and Eastern-European countries [Master’s thesis, Jönköping University]. DiVA Portal. https://www.diva-portal.org/smash/get/diva2:235158/FULLTEXT01.pdf

Malgesini, G., & Giménez, C. (2000). Guía de conceptos sobre migraciones racismo e interculturalidad. Los Libros de la Catarata. https://www.te.gob.mx/MaterialEstudioDefensoriaPE/Libros/1.30.1%20Guía%20de%20conceptos%20sobre%20migraciones,%20racismo%20e%20interculturalidad%20253.pdf

Martínez Pizarro, J., & Reboiras Finardi, L. (Eds.). (2001). La migración internacional y el desarrollo en las Américas (LC/L.1632-P). Comisión Económica para América Latina y el Caribe. https://repositorio.cepal.org/server/api/core/bitstreams/e1b57e53-e21c-46a8-836b-fdf11e808778/content

Mhadhbi, K., Terzi, C., & Bouchrika, A. (2020). Banking sector development and economic

growth in developing countries: A bootstrap panel Granger causality analysis.

Empirical Economics, 58(6), 2817-2836. https://doi.org/10.1007/s00181-019-

01670-z

Nawshin, N., Imtiaz, A., & Sarker, M. S. (2024). Comparative analysis of remittance inflows-international reserves-external debt dyad: Exploring Bangladesh’s economic resilience in avoiding sovereign default compared to Sri Lanka. Arxiv. https://arxiv.org/abs/2410.09594?

Nissanke, M., & Stein, H. (2003). Financial globalization and economic development: Toward an institutional foundation. Eastern Economic Journal, 29(2), 287-308. https://ideas.repec.org/a/eej/eeconj/v29y2003i2p287-308.html

Observatorio Económico, Financiero y Social. (2024, March). Reporte trimestral del sistema financiero: Marzo 2024. Universidad de Lima. https://www.ulima.edu.pe/sites/default/files/page/file/reporte_trimestral_sistema_financiero_marzo_2024.pdf

Opperman, P., & Adjasi, C. K. D. (2019). Remittance volatility and financial sector development in sub-Saharan African countries. Journal of Policy Modeling, 41(2), 336-351. https://doi.org/10.1016/j.jpolmod.2018.11.001

Organización Internacional para las Migraciones & Instituto Nacional de Estadística e Informática. (2015). Remesas y desarrollo en el Perú 2015. https://repository.iom.int/bitstream/handle/20.500.11788/1488/PER-OIM_007.pdf?sequence=1&isAllowed=y

Organización Internacional para las Migraciones. (2020, August 26). Instantáneas analíticas sobre la COVID-19 #53: Remesas internacionales: Actualización. https://www.iom.int/sites/g/files/tmzbdl2616/files/documents/instantaneas_analiticas_covid-19_53_remesas_internacionales_-_actualizacion.pdf

Orozco, M., & Fedewa, R. (2006). Leveraging efforts on remittances and financial intermediation (IDB Working Paper No. 24). Inter-American Development Bank. http://dx.doi.org/10.18235/0011095

Piégay, P., & Rochon, L.-P. (2005). Teorías monetarias poskeynesianas: Una aproximación de la escuela francesa. Problemas del Desarrollo, 36(143), 33-57. https://www.scielo.org.mx/scielo.php?pid=S0301-70362005000400003&script=sci_abstract

Prempeh, K. B., Kyeremeh, C., & Danso, F. K. (2023). The link between remittance inflows and financial development in Ghana: Substitutes or complements? Cogent Economics & Finance, 11(2), Article 2237715. https://doi.org/10.1080/23322039.2023.2237715

Rajan, R. G., & Zingales, L. (2003). The great reversals: The politics of financial development in the twentieth century. Journal of Financial Economics, 69(1), 5-50. https://doi.org/10.1016/S0304-405X(03)00125-9

Ramirez, M. D., & Sharma, H. (2008, junio). Remittances and Growth in Latin America: A Panel Unit Root and Panel Cointegration Analysis (Yale Economics Department Working Paper n.° 51). SSRN. https://ssrn.com/abstract=1148225

Sahay, R., Čihák, M., N’Diaye, P., Barajas, A., Bi, R., Ayala, D., Gao, Y., Kyobe, A., Nguyen, L., Saborowski, C., Svirydzenka, K., & Yousefi, S. R. (2015, May). Rethinking financial deepening: Stability and growth in emerging markets (IMF Staff Discussion Note No. SDN/15/08). International Monetary Fund. https://www.imf.org/external/pubs/ft/sdn/2015/sdn1508.pdf

Saisana, M., & Tarantola, S. (2002). State-of-the-art report on current methodologies and practices for composite indicator development (EU publication No. EUR 20408 EN). European Commission Joint Research Centre. https://op.europa.eu/en/publication-detail/-/publication/9253d939-b47b-4428-b792-619e6b6c8645

Sargan, J. D. (1958). The estimation of economic relationships using instrumental variables. Econometrica, 26(3), 393-415. https://doi.org/10.2307/1907619

Schumpeter, J. A. (2008). The theory of economic development: An inquiry into profits, capital, credit, interest and the business cycle (R. Opie, Trans.). Transaction Publishers. https://www.researchgate.net/publication/272398717_Schumpeter_JA_1934_2008_The_Theory_of_Economic_Development_An_Inquiry_into_Profits_Capital_Credit_Interest_and_the_Business_Cycle_New_Brunswick_USA_and_London_UK_Transaction_Publishers (Original work published 1911)

Stiglitz, J. E., & Weiss, A. (1981, June). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393-410. http://www.jstor.org/stable/1802787

Toasa, H. R. (2016). Las remesas familiares y su impacto en el crecimiento económico en el Ecuador, periodo 2000-2014 [Undergraduate thesis, Universidad Nacional de Chimborazo]. DSpace UNACH. http://dspace.unach.edu.ec/handle/51000/3202

Toxopeus, H. S., & Lensink, R. (2008). Remittances and financial inclusion in development. In T. Addison, & G. Mavrotas (Eds.), Development Finance in the Global Economy. Studies in Development Economics and Policy. Palgrave Macmillan. https://doi.org/10.1057/9780230594074_10

Weerawarna, R., & Miah, S. J. (2023). Empowering remittance management in the digitised landscape: A real-time Data-Driven Decision Support with predictive abilities for financial transactions. Arxiv. https://arxiv.org/abs/2311.11476

World Bank. (2023, December 18). Remittance flows continue to grow in 2023 albeit at slower pace [Press release]. https://www.worldbank.org/en/news/press-release/

2023/12/18/remittance-flows-grow-2023-slower-pace-migration-development-brief

Wray, L. R. (1992). Commercial banks, the central bank, and endogenous money. Journal of Post Keynesian Economics, 14(3), 297-310. https://www.jstor.org/stable/4538297